Many of you have come to realize that the silver price is dependent on base metal miners and their costs of production. This is a graphic explanation of the revenue/income parameters of gold and silver miners. You'll have to adapt the modeling to your own miners, but this presentation does furnish us some insight into where we are in the metals' cycles and the extremes we've gone to, and what we can expect generally going forward. It's a very cheerful future for those holding the real thing.

by SRSrocco on December 22, 2013

by SRSrocco on December 22, 2013

Many precious metal investors today are troubled by the current weakness in the price of silver and are concerned that prices could fall much lower. While the price of silver could continue to fall a bit from here, it's more likely we will see a higher, rather than a lower trend in 2014.

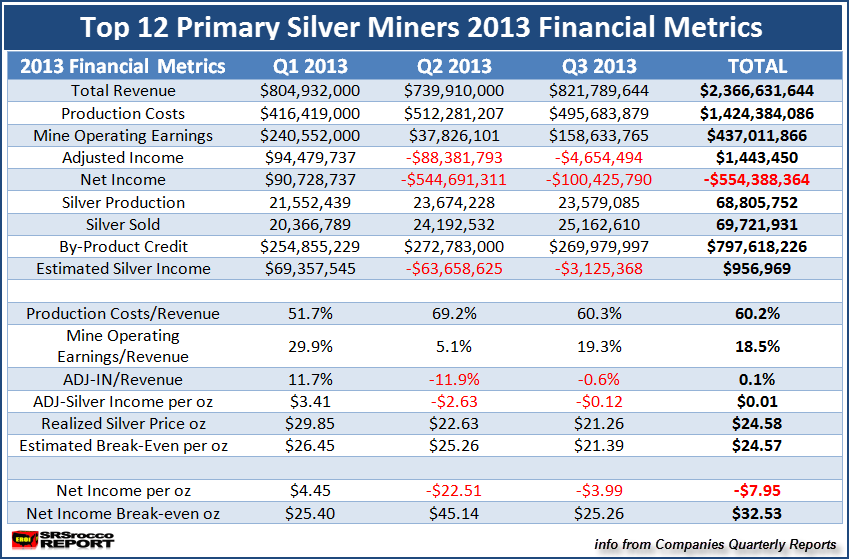

If we look at the table below, we can see the total three-quarters of financial metrics from my top 12 primary silver miners.

By adding up all the figures, we can see some interesting data points. For example, the top 12 primary silver miners recorded a combined $2.36 billion in total revenue for Q1-Q3, while their adjusted income amounted to only $1.4 million.

Thus, the average realized price received by the top 12 silver miners for the first nine months of 2013, was $24.58. Their estimated silver break-even turns out to be one cent less at $24.57.

Even though this is the average for the first three-quarters of the year, the group was able to lower their break-even to $21.39 in Q3. I don't believe the break-even will be much less (and probably higher) due to the fact that the group sold 1.4 million more silver in Q3 than they produced.

Furthermore, the group produced 68.8 million oz of silver for the first nine months of 2013 while they sold 69.7 million oz. I highly doubt they will continue to sell more silver than they are producing for the next several quarters.

It is quite amazing to see that these 12 primary silver miners had $2.36 billion in revenue during the first nine months of 2013 while only showing $1.4 million of adjusted income. The power of the FED is mighty indeed. The net income of a negative $554 million for the Q1-Q3 was due to the huge write-downs during the second quarter.

The Price Of Silver Is Below The Group Average Cost of Production

The current price of silver is $19.40, while the estimated break-even for the top 12 primary silver miners in Q3 was $21.39. According to Kitco, the average price of silver so far in Q4 is $20.76 or 63 cents less than the prior quarter.

I imagine we may see continued losses from the group in the last quarter as the miners receive a lower price for their silver and as stockpiled silver sales are reduced. However, there is a chance that we may indeed see a small gain for the group in Q4 if the by-product revenues increase due to stronger prices for copper, zinc and lead (Q over Q) and costs continue to decline.

The Low Price Of Silver & Market Sentiment

This chart from Shortsideoflong.com, shows both the price of silver and public opinion of the shiny metal.

Here we can see that sentiment is now approaching the lows seen in June of this year. What we have taking place are market sentiment lows as well as the price of silver below the break-even for the top 12 miners.

Yes, it's true that most of the silver comes from by-product mining, however I have checked the break-even for Hecla and Coeur back in 2000, and I honestly say… the price of silver was not much lower than their break-even at the time. So I doubt we will see much lower prices for silver.

The Fed and member banks are not that stupid to push the price of gold and silver too far below their break-even as it would as it would force investors to take more physical bullion off the market.

If we look at the next series of charts we can see just how much gold and silver have under-performed the commodity index:

The Dow-Silver ratio has increased 3.3 times since the low in August of 2011, The Dow-Gold ratio is 2.3 times higher than its low in August 2011, and the Dow-CCI – the Commodity Channel Index has only increased 1.8 times since the same time period.

How Jeff Christian can brush off gold and silver manipulation while the Fed & Central Banks prop up the entire market with $Trillions of liquidity makes you wonder why he fails to mention that a good part of his business is in Precious Metal Paper Derivative-Hedging.

You see, the huge rise in the price of silver since 2005 has been due to Investment, not Industrial Demand. The price of silver remained below $5 since the late 1990′s even though there was a silver supply deficit.

So, if you have your head screwed on correctly, the only way to destroy the price of silver is to crush INVESTMENT DEMAND….. period. Hence, the work of the FED and member banks.

I have to tell you… its hard to hold my tongue as I read and listen to some of the worst analysis to come out of alternative media…. forget MSM. I am talking about the folks who are supposed to be part of the alternative media.

A good percentage of the energy analysis that comes from some of the well-known subscription services is absolutely atrocious. You know exactly who I am talking about. I am completely taken-back by how much the New Shale Energy Revolution is being hyped as our new savior on the alternative media...Read more @Source